Taxes are an unavoidable part of life, but understanding how they function can make the system less confusing. One important concept in the U.S. tax system is the structure of tax brackets, including the lower ranges. This post explores what these brackets are, how they operate, and the 2026 federal income tax thresholds.

What Are Tax Brackets? The Role of Lower Rates

A tax bracket is a range of income taxed at a specific rate. The U.S. uses a progressive system, meaning income is taxed at higher rates as earnings increase.

The lower portions of income are taxed at the smallest rates, often referred to as the entry-level or lower brackets. For example, in 2026, the lowest federal income tax rates are 10% and 12%. These initial segments of income are taxed at these rates, while higher income is subject to higher percentages.

It’s important to note that reaching a higher bracket does not retroactively tax all income at that rate. Only the amount above the threshold falls into the next bracket.

2026 Federal Income Low Tax Brackets

For 2026, the IRS defines seven federal income tax rates. The two lowest rates apply to the first portions of taxable income:

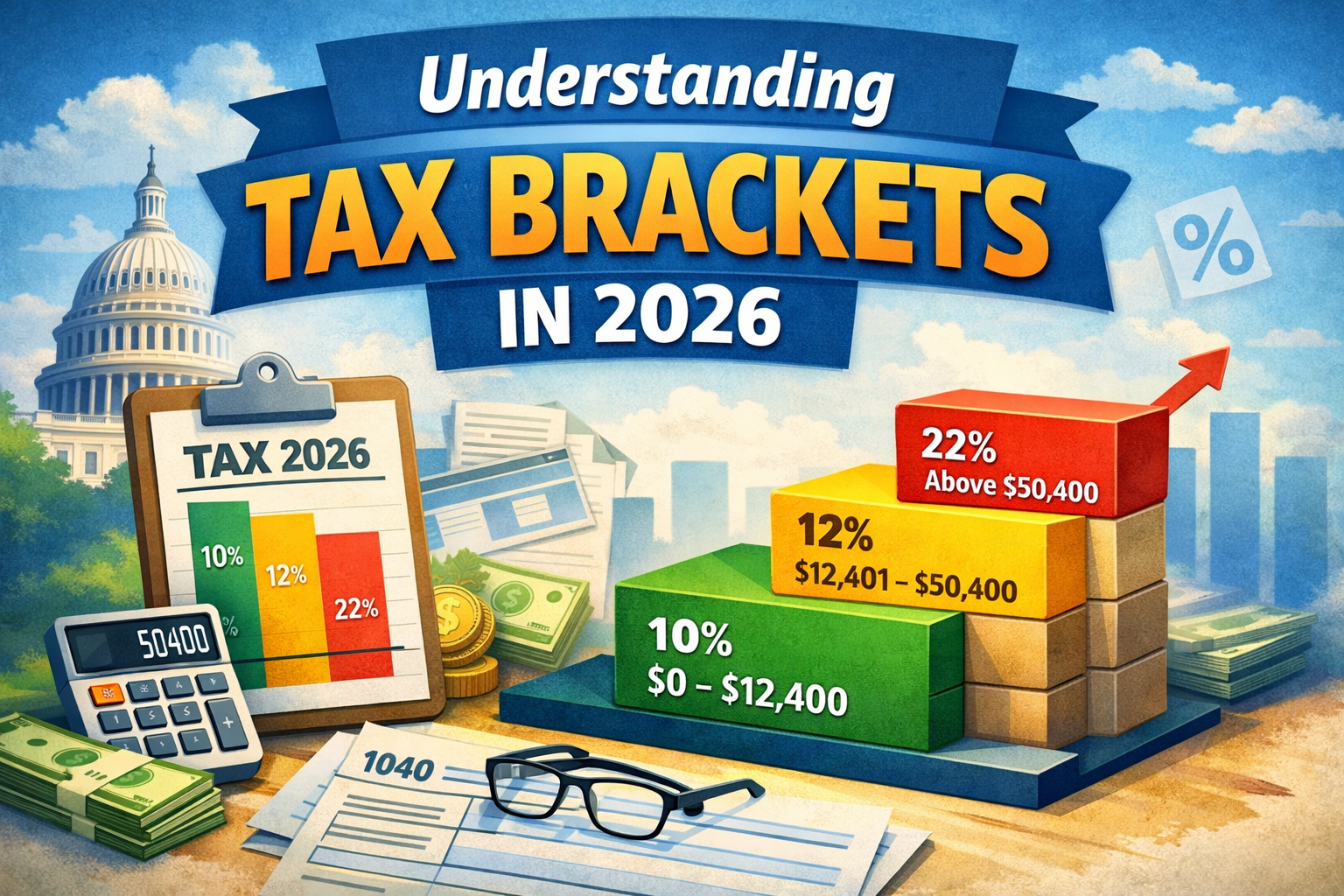

Single Filers

- 10%: $0 to $12,400

- 12%: $12,401 to $50,400

Married Filing Jointly

- 10%: $0 to $24,800

- 12%: $24,801 to $100,800

Head of Household

- 10%: $0 to $17,700

- 12%: $17,701 to $67,450

These ranges represent the earliest income segments taxed at federal rates.

How Marginal Rates Work

The U.S. tax system is marginal, meaning each rate applies to a specific slice of income. A single filer earning $60,000 in 2026 would see their income divided into brackets:

- 10% on the first $12,400

- 12% on the next $38,000 ($12,401 to $50,400)

- 22% on the remaining $9,600

This structure shows how the initial income segments benefit from the lower percentages while higher income is taxed more heavily.

Impact of Standard Deductions

Taxable income is calculated after deductions. In 2026, the standard deduction amounts are:

- Single filers: $16,100

- Married filing jointly: $32,200

- Head of household: $24,150

Deductions reduce taxable income, which determines how much of earnings are subject to the lowest rates. A single filer with $50,000 in total income would have a taxable income of $33,900 after the standard deduction, keeping a significant portion in the lower federal brackets.

Capital Gains and Lower Rates

The concept of marginal brackets also applies to long-term capital gains. In 2026, the 0% capital gains rate applies to income up to certain thresholds, similar to the early brackets. For single filers, this threshold is roughly $49,450, meaning income below this level is not taxed on long-term gains.

This demonstrates that the initial portions of taxable income influence not only wages but investment earnings as well.

Common Misconceptions

Several misunderstandings surround these lower tax brackets:

- Higher brackets do not apply retroactively to all income. Only the income within that bracket is taxed at the higher rate.

- Lower brackets are not indicators of poverty or earning potential. They simply represent the first taxed segments.

- Marginal rates differ from effective tax rates, which are calculated across total income.

Understanding these distinctions clarifies the purpose of the early-rate brackets in a progressive system.

Comparison of Low Tax Brackets by Filing Status

Lower tax rates vary based on filing status. The thresholds for married couples filing jointly are higher than those for single filers, reflecting shared household income.

| Filing Status | 10% Bracket | 12% Bracket |

|---|---|---|

| Single | $0 – $12,400 | $12,401 – $50,400 |

| Married Joint | $0 – $24,800 | $24,801 – $100,800 |

| Head of Household | $0 – $17,700 | $17,701 – $67,450 |

These differences ensure that lower rates are scaled appropriately across different household types.

Historical Context of Low Tax Brackets

Lower rates have been part of the federal income tax system since its inception. Initially, the first income segments were taxed minimally to cover basic government revenue while leaving most income untaxed. Over time, thresholds and rates have been adjusted for inflation and policy changes.

Today, these early segments continue to serve as the foundation of the U.S. progressive tax system, providing a lighter tax burden on initial income.

Marginal vs. Effective Rates

Marginal rates apply to the last dollar earned within a bracket. Effective rates reflect the average rate paid on all income. For a single filer earning $50,000 in 2026:

- Marginal rate: 12%

- Effective rate: Approximately 9–10%

The early-rate brackets are central to understanding the difference between marginal and effective taxation.

Summary of Key Points

- The initial segments of income are taxed at the lowest federal rates.

- In 2026, the lowest rates are 10% and 12% for most taxpayers.

- Filing status affects the thresholds of these early-rate brackets.

- Deductions and taxable income influence how much income falls into these segments.

- These early brackets form the foundation of the progressive tax system, with higher rates applying to additional income.

Conclusion

The lower segments of federal income tax brackets define the earliest portions of income that are taxed at the smallest rates. In 2026, these entry-level rates are 10% and 12%, and they affect wages, investment income, and the calculation of effective and marginal rates.

Understanding how the early segments work provides clarity on how the U.S. tax system structures income taxation and how thresholds vary across filing statuses.